The last two decades have seen the use of standardized Technical Reports disclosing technical and economic results for exploration and mining projects around the world. For projects located in Canada, or Canadian companies that operate worldwide, Technical Reports are prescribed by Canadian National Instrument 43-101 – Standards of Disclosure for Mineral Projects (NI 43-101). However, companies based outside of Canada are filing NI 43-101 reports as well. Furthermore, technical reports are also being written in accordance with the Australasian Code for reporting of exploration results, mineral resources and ore reserves (JORC Code), South Africa (SAMREC) and other international codes of practice.

The last two decades have seen the use of standardized Technical Reports disclosing technical and economic results for exploration and mining projects around the world. For projects located in Canada, or Canadian companies that operate worldwide, Technical Reports are prescribed by Canadian National Instrument 43-101 – Standards of Disclosure for Mineral Projects (NI 43-101). However, companies based outside of Canada are filing NI 43-101 reports as well. Furthermore, technical reports are also being written in accordance with the Australasian Code for reporting of exploration results, mineral resources and ore reserves (JORC Code), South Africa (SAMREC) and other international codes of practice.

While there has been widespread adoption of standardization in Technical Report preparation, the quality of the reports can vary widely. This variability and the lack of standardized metrics from report to report has led some to imply that the use of misleading methods, biased practices, or other deficiencies is common, that mining companies and/or their consultants are not following regulated reporting standards, and so the evaluation of potential economic viability of projects is rendered unreliable.

NI 43-101 Technical Reports for Canadian-listed mining companies are posted on SEDAR. The posting of a report on SEDAR does not imply that the report has been reviewed for compliance by the various Canadian regulators. Indeed, the authorities have periodically raised concerns about the number of reports filed that are subsequently found to be deficient. These deficiencies range from a relatively minor technicalities all the way up to fundamental errors, such as reporting resources without applying a cut-off grade.

Some companies or individuals writing NI 43-101 style reports display a general lack of understanding as to what constitutes compliance with NI 43-101. It appears that reports written by companies or individuals based outside of Canada are more often deficient.

However, even a report that is fully compliant with NI 43-101 may not have the metrics needed to be able to compare projects because, while the contents of NI 43-101 Technical Reports are prescribed, the Qualified Person(s) writing the report has the responsibility of determining the materiality of the scientific or technical information to be included in the report. Moreover, the NI 43-101 Technical Report merely summarizes the relevant material technical and economic information for a property or project; it is not intended as a collection of all the available data. In fact, while NI 43-101 does require that particular items are discussed in each chapter, it is up to the Qualified Person (QP) as to how best to present the information in order to provide a comprehensive summary of the project information that remains understandable to the layman.

Variability between Technical Reports can result of the choice of metrics and methodologies which a QP uses to estimate a resource, for example. That choice is based on their experience, but also takes into account the client’s knowledge of the project or deposit and their preference regarding the mining method, processing method and overall size of the operation.

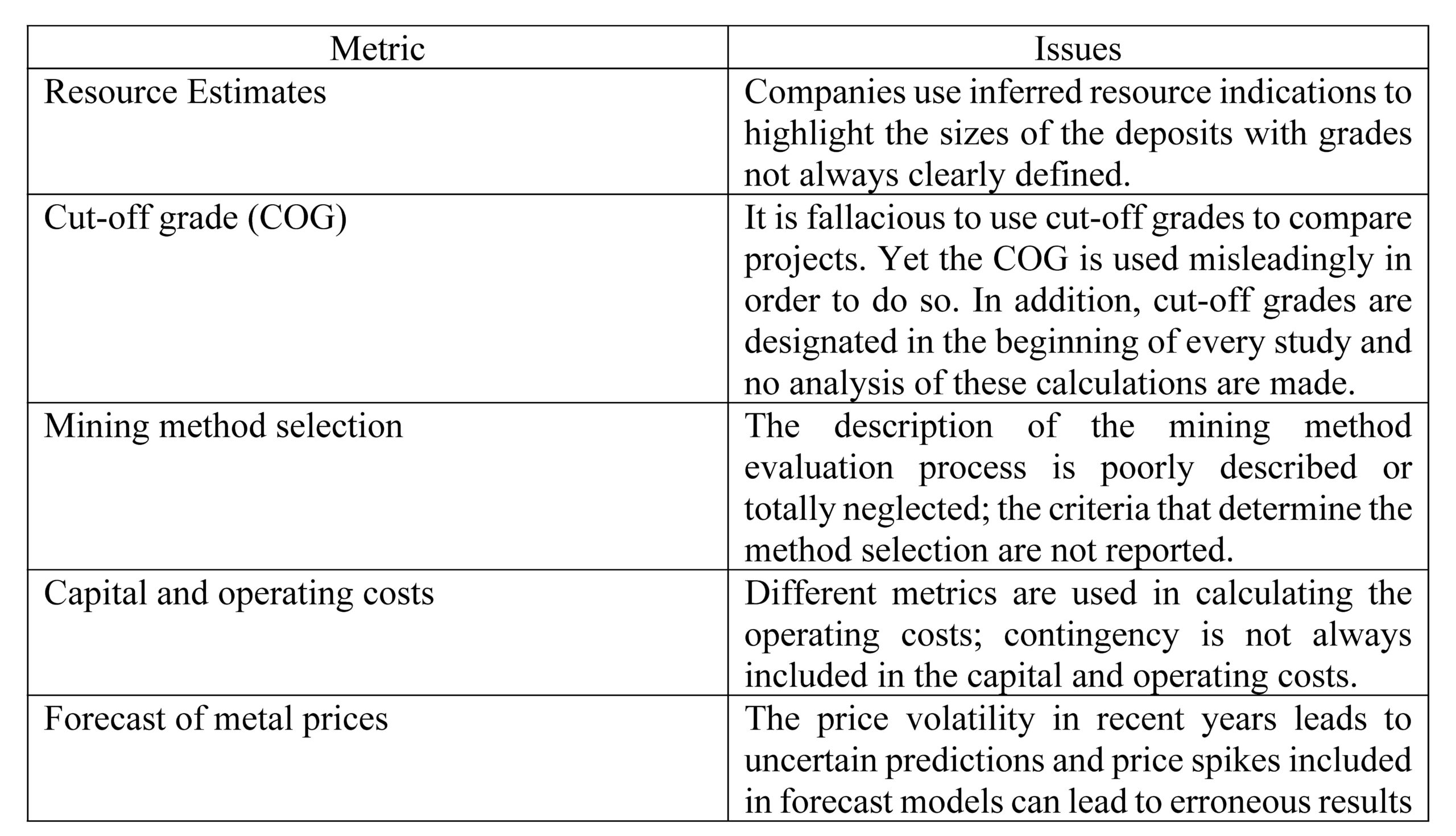

Some of the common issues regarding the metrics in studies are summarized in Table 1.

Table 1

Issues Regarding Metrics in Studies

Resource Estimates in Economic Studies

The use of inferred resources is limited to a Preliminary Economic Assessment (PEA) or Scoping Study which are preliminary in nature and include only a very basic study of the potential economics of a project. These studies are usually not intended to provide comprehensive detail because they are based in part on unproven assumptions regarding the geological and technical aspects of the project. These studies have a high degree of uncertainty in operating and capital cost estimates along with other variables and serve only to illustrate the potential for viability of the project, often based on inferred resources. It should be expected that many or all of the assumptions in a PEA will be substantially changed as the project advances. Nevertheless, a Technical Report describing the results of a PEA establishes potential viability of the project and so has traditionally been used a milestone, on the basis of which funding for further development of the property can be raised, or the property itself may be sold.

Investors also need to recognize that the use of inferred resources in a PEA always carries a risk and that the next drilling program could radically change the outlook of a project in terms of resource tonnage and/or grade. Naturally, any positive bias in the Inferred resource estimate would tend to result in a downward correction when that resource is converted to Indicated or Measured resources.

A comparison of PEA studies for similar projects highlights the wide range in level of detail incorporated into these reports. Such reports range from data-poor to very detailed. However, while an increase in the level of detail (i.e. quantity of work) incorporated, into a PEA should de-risk the project to a certain extent on the part of the investor, this is not always the case. The actual risk may be much higher than it appears because the quality of the work conducted was poor. Therefore, an investor assessing the level of risk in a project which has had a PEA study conducted on it should look at the quality rather than the quantity of work conducted on the project. A reviewer or investor must also remember that, because the PEA allows for the inclusion of inferred mineral resources into the production plan, the economic portion of the study can only indicate the potential outcome should the project succeed.

As both Pre-Feasibility and Feasibility Technical Reports are only allowed to use measured and indicated resources when conducting any economic studies, these studies should have less risk than a PEA. This is correct, provided the mineral resource estimates reflect a good understanding of the geological and mineralogical controls, and are reported at a cut-off grade based on appropriate economic parameters. The mining and processing methods, recoveries, capital and operating costs as well as any marketing and environmental and social issues all need to be well understood.

An inherent problem is that, in a number of cases, as soon as positive results are published for the PEA, the companies want to commence a Feasibility Study without completing any intermediate engineering studies or they rush to complete these technical studies in the least amount of time. The failure to conduct the intermediate engineering studies can lead to increasing risk for the project because it eliminates an important de-risking phase from the development process. Importantly, the pre-feasibility phase allows for trade-off studies for various mining and processing options to be evaluated rapidly at relatively little cost. The results of the pre-feasibility study would then be used to determine the best options to use as the basis for the Feasibility Study.

Cut-Off Grades (COG)

Investors in the mining industry sometimes use cut-off grades to benchmark projects. In respect of mineral resource estimates or PEAs, though, there is a large measure of uncertainty involved in the underlying estimates and assumptions, making COG risky to use as yardstick for comparison. As projects advance, the data become more comprehensive, and the cut-off grade can be calculated with greater confidence, at which stage a comparison of the break-even cut-off and average reserve grade can provide a fair indication of potential operating margin. However, a valid criticism some studies has been that they do not provide a breakdown or analysis as to how the COG was derived. Subsequent revisions of the reporting standards have recognized this, and it is now recognized as best practice for Technical Reports to include this detail.

In basic terms, the break-even cut-off grade can be determined by the following formula:

Cut-Off Grade = Operating cost per unit / (Metal Price per unit x Processing Recovery)

Operating costs and metal prices for many commodities are stated on a USD/unit basis (e.g. $/oz, $/lb, $/t) using either USD or local currency. Processing recoveries may be based either on the metallurgical testwork for the project or actual recoveries for the processing plant.

Investors appear to focus particularly on the grade of a deposit as the indicator of potential profits. Operating costs, however, can be extremely variable from project to project since they are dependent not only on unit costs for labour, electrical power, shipping costs, etc. but also on exchange rates, the grade of material sent to be processed, the process flowsheet, and scale of operation. Moreover, the mining and processing methods employed to extract ore from the deposit, open pit stripping ratio, equipment selection, process recovery or product transport costs can lead to higher grade projects providing lower returns than lower grade deposits.

Therefore, extreme caution is needed in using COGs to compare projects except perhaps when dealing with very similar mines in a particular region or district.

Mining Method Selection

Generally, the orientation, width, strike length, depth of the overburden, overlying geographical features and geohydrological or geomechanical are all features that are considered when deciding on the mining method.

As a PEA is a very preliminary study of the potential economic nature of a mineral deposit the mining method selected for the study is usually the one(s) that appears to best fit the available data at the time of the study. Later work may confirm this or may substantially change the mining method.

In more advanced studies such as a pre-feasibility or feasibility, a company may have conducted trade-off studies that optimized the mining rates or the mining method that are not discussed in the NI 43-101 since the technical study used the optimized rate or method as its basis. In these cases, the QP may not have noted any trade off studies in the report as the studies were not material to the project. As an NI 43-101 Technical Report is a summary of the data and study findings that are material to the project, tradeoff studies are usually part of the work that underlies final study and references to them may be either found in the appendixes or noted in the bibliography.

A Technical Report that has an economic study attached to it needs to discuss the mining method envisioned for the project, but NI 43-101 does not require the QP to discuss why a particular mining method was chosen only that chosen method is described in some detail. The QP may refer to any trade-off studies or may not discuss them at all if they have no material impact project.

There has given rise to some adverse commentary regarding lack of detail in Technical Reports in relation to the mining method selection. This is a valid observation, as often this has been poorly described or totally neglected, so that mining method selection criteria are not described. This may arise when the client has stated a preference for selection of a particular mining method.

Capital and Operating Costs

A barrier to comparing projects based on their Technical Reports is that different metrics may be used in calculating the capital and operating costs. Thus, costs may be expressed per tonne of ore treated, per tonne of concentrate sold, or per tonne (or ounce) of payable metal.

While the standardized technical reports require the QP to discuss both the capital and operating costs each firm or QP has their own way of organizing this information and will select metrics that are most appropriate to that particular project. Also, while the report should reflect the level of detail in the underlying work, the QP may choose to combine categories of cost into broader headings. It would be a pity to sacrifice this flexibility in the cause of standardization.

In respect of some specialty minerals, privately-owned industry leaders may be reluctant to share proprietary information, making it harder yet to compare projects or try and determine the costs associated with a similar project.

This being said, a PEA study may present a forecast of costs based on nearby analogous projects, or similar projects elsewhere in the world. However, operating mines rarely disclose their cost breakdown in public reporting. Consequently, PEA cost estimates may depend on a number of projects or sources that are not always disclosed, whereas later studies will typically require a zero-based estimate and in a feasibility study the cost estimates should be based on rates or quotes from established contractors, suppliers or manufacturers.

Once again, as the Technical Reports summarizes the work conducted as part of the overall study, precise details or sources of the costs may not be disclosed in the report but would form part of the body of work which underlies the Technical Report.

Metal Prices

As with other types of forecast, the reliability of metal price forecasts falls significantly as the time period increases, and there is every reason to expect that this pattern will continue. Even predictions based on market supply and demand data may prove unreliable in predicting the long-term metal prices. A base case metal price is necessary, though, to understand the economic nature of a project at a given time. In addition, Micon considers it beneficial to provide a table showing sensitivity of the project to changes in the metal price. This allows the reader to better understand the effect of swings in metal prices on the overall project.

Conclusions

While the use of standardized Technical Reports for exploration and mining projects around the world has become the norm, there is still a wide variety in the quality of the reports. This variability and the lack of standardized metrics from report to report has led some to imply that there are misleading methods, biased practices, or other deficiencies when evaluating the potential economic viability of projects, or simply that mining companies and their consultants are not following the regulated reporting standards. We do not consider that to be true.

Just as no two mineral deposits are entirely the same, no two reports will be the same even when using standardized reporting. Any difference in metrics used in Technical Reports should not lead one to imply that the QP has applied misleading methods, biased practices, or other deficiencies, or that a Technical Report falls short of the regulated reporting standards.

Variation in the metrics applied between Technical Reports is a consequence of the QP selecting the most appropriate metrics for that project based on their experience. Chosen wisely, these should assist the reader in understanding risk inherent to mining projects and Micon considers that QPs should not be overly constrained by the need to standardize metrics in their reports.

The QP is personally responsible for determining the materiality of the scientific or technical information to be included in the Technical Report. An NI 43-101 Technical Report summarizes the relevant and material technical and economic information for a property or project and should be written such that it is understandable by a layman stock investor. Most deficiencies appear to result from a lack of familiarity with the requirements of NI 43-101 and the expectations of regulators in terms of best practice guidelines. Choose your QP wisely!

.

.

.

.

.

.

.

0 Comments